Quarterly Strategic Review - 1st Quarter (Jan-Mar, 2024)

First Quarter 2024 – April, 2024 – Is It Only The Start?

A Strong Rally in Our Accounts

We have continued to participate in the strength of risk assets, and particularly the likes of U.S. stocks, Bitcoin, and more lately gold. One of the major topics of discussion that came about at the CMT Association Summit in Dubai when I was recently there was what if equities (stocks) are only now getting started? What if the recent breakouts in world equities, European equities, and the fact that even the S&P 500 only recently surpassed its 2021 highs this past quarter suggests we’re closer to the beginning/early innings of a broader asset price rally that will offer steady opportunities to make productive use of our assets? Technically, I have to say, I have firmly embraced this possibility and know that many would be caught offside. The fact that we have been willing to be trend followers and not let our opinions or concerns (or the narratives pitched by the sensationalist media bent on creating fear) get in the way is bearing financial fruit.

The fact that in late March, and now into the 2nd quarter, we’re seeing the expansion of opportunity as commodities re-ignite and are no longer only an entertaining cocoa story is important. Seeing the mining stocks, the precious metals, the energy stocks, uranium and base metals add some depth to the technology/communications story is very good news for investors. And seeing some strength, absolutely at least, out of U.S. mid-caps and even small-caps suggests the market is getting stronger (not weaker).

Interest Rates and Inflation

You will recall that since the bottom in the interest rates, I have suggested that the 40-year downtrend has ended, and investors are going to take some time adjusting to the new generational environment that we have entered. Used to spending more money than we have and encouraged by our banks who’ve created an almost normalcy around the idea of paying down your mortgage, and then borrowing it right back via a line of credit for that renovation or vacation you’ve dreamed of is causing turmoil to many young families who are realizing they’re in a system that doesn’t necessarily look out for their interests.

I repeat, I’d continue to encourage all of us, whether you’re in your 20s right through to 80s+, to carefully consider financial commitments. If older, it can be speaking to your grandkids. If younger, it can be thinking twice before making decisions that will only work out in your favour if “X” happens. For example, if perhaps “X” happens to be interest rates/mortgages rates/etc. will fall. In the new era of higher interest rates, some see that as an opportunity to earn more on their money than in the past, but I’d again urge you to realize that the fact that interest rates are what they are, suggests that higher returns are available elsewhere (and we need to take advantage of opportunity when and where it exists).

With what I suspect to be sticky inflation (higher and more persistent than expected), an increasing probability of future supply shocks and a world that, for the most part, continues to live irresponsibly spending away generations of future potential to live for today, commodities rising from here will push inflation higher and further diminish the likelihood of central bank action to decrease rates. That would be too risky. And while the idea of earning 5% on your money sounds good (compared with the past 10-years), equities are providing much more than that at this juncture and continue to be one of the benefactors (of many) of all that monetary excess. For every government program you hear of, whether Canada’s proposed UBI (universal basic income), or subsidies paid to recently immigrated folks, it’s money that gets spent in the system. If every Canadian were to suddenly receive $24K/year (proposed plan), it would be like nobody got the $24K in the first place. The limited goods would be purchased, and prices would rise by the full amount, providing nothing but accelerating debt burdens placed upon the future and the citizens that thought they were being helped, would be even worse off. Be careful what you wish for.

Gold is Finally on the Move

Only recently, gold has begun to push more firmly above levels first reached 13 years ago in 2011. Gold has, over time, offered long-term inflationary protection and the ability to outpace the gains of prices and as such, rightfully earned its reputation as a store of value. We’ll be watching carefully to see if the trend of gold prices vs. stock prices can move higher and actually outperform. In case you don’t know, it’s the countries of the east (i.e., China & Russia) that have been buying, acquiring, and owning big proportions of gold all whilst the western world borrows and continues its debt binge. Canada is one of the few countries that owns essentially zero gold in its treasury. Oops. Almost as poor of a decision as when the U.K. government sold all their gold reserves at multi-decade lows at the turn of the century (’99-’02) around $250.

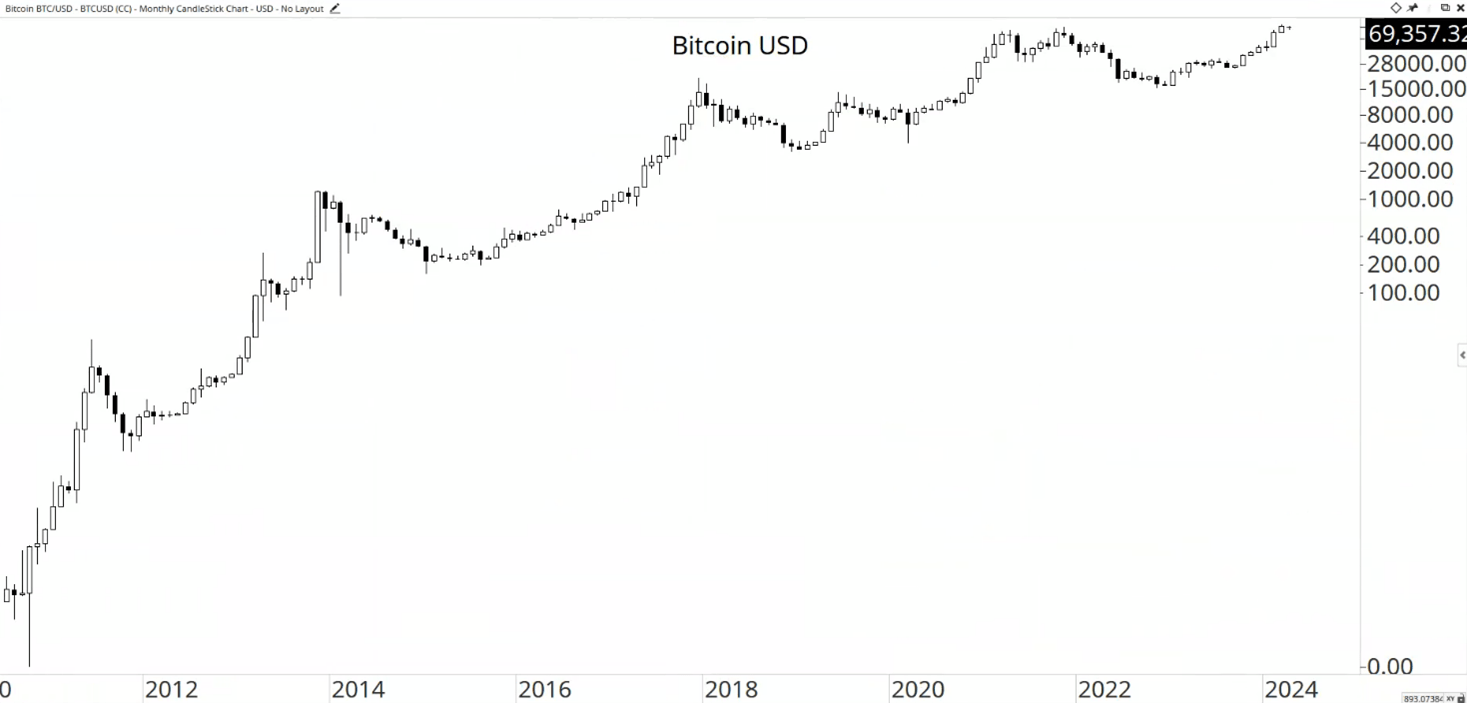

But digital gold is here, and the case for Bitcoin is growing. The new demand from ETFs has been large, and more consistent than market expectations. You see, with a finite supply available and a large new buyer (the ETFs have amassed a new $12.1 billion in the past few months), you have a recipe for higher prices (Bitcoin is ~+60% from last quarter when I wrote on the topic). And higher prices inevitably capture attention, and attention brings on new interest and new interest brings on higher prices and so forth. But prices (of any asset!) at some point get out of hand and can (and will) deal a lesson to those who chase and act irrationally. This happens with every bubble, whether in real estate, technology stocks, or silver (or tulips for those of you that know history). We always have to observe price action and orderly price movement is indeed more ideal than erratic and wide swings in demand and supply. While some would be tempted to say the swings in Bitcoin meet that erratic definition, when you zoom out and look at the long-term monthly chart, all you really see is what looks like an orderly uptrend over time. The strength since the fall of 2022 at this point certainly doesn’t look unusual or bubble-like.

Source: Optuma

Don’t We Like Dividends Yet?

No, we don’t. While I’d certainly agree with anyone that suggests the stock market doesn’t always make sense, I would continue to encourage you to realize that dividend stocks aren’t supposed to like an environment of higher interest rates. As such, they’re underperforming (and this makes sense!). Since we are flexible, nimble and have such a wide set of options to us at the helm of stewarding your investment assets, dividend stocks simply don’t make the cut. That’s not to say there aren’t stocks that we hold that pay a dividend, but if the trend of interest rates is indeed what I’m suggesting it appears to be, then dividend stocks aren’t something we want to be overly exposed to. Opportunity cost is important. Even if we forget about opportunity cost, let’s not forget about risk management and anytime we buy or own a stock, or asset that is more volatile than an alternative (made worse if it’s not rising), we do ourselves a disservice in our portfolios. If the stock isn’t doing better than the sector ETF, we should own the sector ETF. If the sector ETF isn’t doing better than the market itself, we should own the market. If the market we’re investing in isn’t doing better than a different market (a different place in the world), we should go there. That’s how we operate. We will continue to do that in our accounts.

Our Strategy and Positioning

Overall, we remain overweight of stocks in the accounts of all clients in the balanced risk buckets, and while an equity only client typically sees some cash laying around, it’s really just for the next opportunity, and not sitting around costing us opportunity. Even in the context of the current market environment, which has rewarded us, individual stocks still give up and peak out, creating opportunities to take profits and some new positions don’t work out as planned, requiring us to cut losses. That’s all part of following our process.

On the whole, we have mildly decreased exposure to our overweight technology stance and have increased exposure to base metals (copper/steel/etc.), energy (oil/uranium), and industrials as these rotations develop. These changes and portfolio adjustments are the natural consequence of market behaviour and not something to be afraid of. To see different types of stocks provide buy points, relative strength, and opportunity is good thing.

At this point, pullbacks are to be bought and what this market is doing is providing very few of those. Those that chose to get off the equity uptrend are finding themselves on the outside looking in. Creating excuses about potential recessions, election turmoil, or new wars as a reason to not stick with the market uptrend is risky in itself. Stocks provide inflationary protection and are supposed to go up in times like this – it makes sense. It’s only those with assets like stocks, gold and Bitcoin in countries that are experiencing massive inflation (like Argentina and Turkey) that are maintaining some hope of future purchasing power. The rest, sadly many/(most?), who don’t have the capital to invest fall further and further behind. It’s not fun and doesn’t always seem fair, but there are consequences to financial decisions, both ours and our governments’.

As usual, I’ll ramble further with some visuals in the more detailed supplementary strategic review that will be out later in April.

Sincerely,

David Cox, CFA, CMT, FMA, FCSI, BMath

Senior Portfolio Manager, Wealth Advisor

Raymond James Ltd.

Phone: 519.883.6031

Unit 1 – 595 Parkside Drive | Waterloo, ON | N2L 0C7

david.cox@raymondjames.ca

www.financiallyinsync.com

![]() @DavidCoxRJ

@DavidCoxRJ