Quarterly Strategic Review - 2nd Quarter (Apr-Jun, 2024)

An Uptrend Through Choppy Waters

Since the bottom of the stock market in the fall of 2022, we have remained steadfast in our desire to hold equities and express a bullish, optimistic outlook in our portfolios. The U.S. market is still, without question, the global leader, but it’s experiencing a correction underneath, while the rest of the world continues to try to improve. This past quarter was much more challenging due to the weak market breadth, which most simply means fewer stocks continued to rise, despite an index like the S&P 500 going up. The S&P 500 index has been driven disproportionately by those big stocks like Nvidia, Apple, Microsoft and Google.

In fact, $NVDA, $MSFT, $AAPL, $AMZN, $META and $GOOG have been 65% of the YTD return in the S&P 500… In hindsight, we haven’t had enough of these, this past quarter, to keep up.

Is the market in trouble because of the weak breadth? No, I don’t see it like that (yet), but always need to acknowledge there are definitely some warning flags that exist, and one of two things could be expected to happen. Firstly, a number of stocks that have been quietly correcting downwards in recent months could receive new buying interest and start to rise, this would improve the market breadth. Secondly, the big stocks like I just mentioned could instead succumb to selling pressure and the indices could start to weaken. Investing isn’t about certainty, and yet our process is certainly capable of providing us with a pulse on the market conditions to make necessary adjustments.

Choppy Means Turnover

This past quarter, it was the more aggressive clients that fared worse. It wasn’t a bad quarter, but many of us experienced small losses, even while the market rose. And there were more stocks that we had to “stop out” of, which means cutting our losses and/or taking our gains. You see, individual stocks are just that, volatile. The index is much less volatile. So, as aggressive investors, we own less of those big stocks that come from our “INsync Universe,” and more stocks breaking out and/or offering more explosive buy points. But the activity didn’t pay off. I’ve done considerable thinking and analysis into this current environment (and whether it’s recognizable, perhaps like 2021?) and will share my findings in more detail in the supplementary review, which will follow in another week.

Outside of those of us who are more aggressive, it was another good quarter, albeit again, tricky to outperform the market with the stocks we did own. The market was very weak in April, then bounced back in May, only to continue in June, though driven by only a few. The stocks we’re sitting on look really good, but that’s not to hide the fact that some prior leaders have turned lower and broken down. Areas like the homebuilders (D.R. Horton and PulteGroup), the transports (Old Dominion Freight Line) and others have faded away. And, knowing that the market is aging and that we’re in the summer period with declining breadth, there is no time to question why stocks are falling. The stocks that continue to trend upwards, especially those that do so relatively (by outperforming the S&P 500) are kept, and others are managed carefully and pruned, amidst the chop.

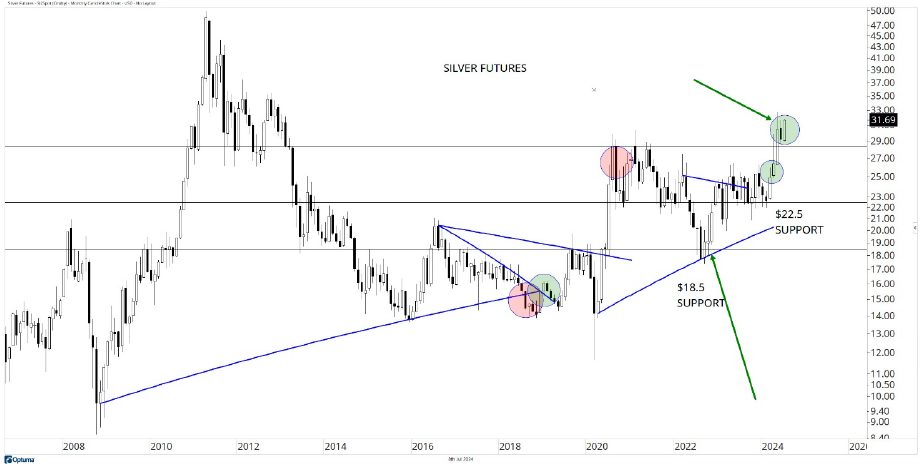

Silver Is Stronger Than Stocks

Last quarter, I talked about gold finally firming up and heading upwards, and that remains true. Gold has not only provided us with some diversity (and portfolio stability), given its low correlation with stocks, but it’s been adding value too. But the recent multi-year breakout in silver looks very big-picture promising. Somewhat surprisingly, we still haven’t seen any signs of robust buying demand in the precious metals stocks, so we have to just accept that they’re more volatile anyways. Some of you own the Central Fund of Canada (think of that as 50/50 gold and silver) and we definitely were a buyer of silver bullion this past quarter too, on the whole. I spoke about silver when I was on BNN in Toronto back on April 22, 2024.

As at: July 8, 2024

Ignore the Media Speculation About Interest Rates

I’ll remind you, that years ago, when interest rates bottomed, the analysts and media pundits missed calling a new trend. They were wrong about how long, and how far, the central banks (all around the world) would go in raising rates. And now, for the past 12-18 months, they’ve tried to play the opposite game of guessing (forecasting/predicting) how far and how quickly the short-term interest rates (the ones controlled by the Bank of Canada and Federal Reserve) will go. But wrong again. They’ve been wildly and blatantly wrong. Sure, Canada did take the lead in reducing the short-term rates by 0.25%, recently, but in the context of how far up they’ve come, that’s absolutely insignificant. The Canadian economy has more than a headwind or two, as the massive immigration has driven demand for houses and rents higher, the monies offered to illegal migrants as a stipend has added to soaring deficits and the impact on borrowers (government, corporations, and individuals) hasn’t been felt yet. All these mortgages will be coming up in the next year or two and barring a huge move back downwards (you know I don’t see this happening), there is going to be more supply of unaffordable real estate hitting the market.

The government is hesitant to prudently force lending standards to tighten, has recently allowed developers to extend term on financing and there is lots of real estate now owned that is underwater by the buyers since 2020. It all adds up to some trouble ahead. That, of course, could be why the Canadian stock market continues to disappoint and remain a weak market compared with markets all over the world. But please remember, in inflationary environments, fuelled by government borrowing, spending and excess, asset prices like stocks and other risk assets are expected to rise and we’ll continue to stick with the trends that remain underway and identify the new ones.

Our Strategy and Positioning

Despite the breadth correction, we remain long of stocks (and overweight, compared with fixed income) for all clients. The technology, communication and consumer discretionary sectors are continued areas of focus and strength, and, along with gold, silver and some Bitcoin and crypto-related securities, rounds out our current approach to portfolio structure.

Owning large-cap stocks from the #INsyncUniverse, the ones that have a history of outperforming and boast a 10+ year chart going from the lower left to the upper right, makes sense, and these same stocks are suitable for aggressive and balanced clients alike and provide great portfolio anchors. We remain open-minded to the short-term correction risk at this stage of the summer, but anticipate that any short-term weakness, would be in the context of a longer-term buying opportunity. Looking ahead, more global equity exposure is a possibility.

Sincerely,

David Cox, CFA, CMT, FMA, FCSI, BMath

Senior Portfolio Manager, Wealth Advisor

Raymond James Ltd.

Phone: 519.883.6031

Unit 1 – 595 Parkside Drive | Waterloo, ON | N2L 0C7

david.cox@raymondjames.ca

www.financiallyinsync.com

![]() @DavidCoxRJ

@DavidCoxRJ

Disclaimer: Information in this article is from sources believed to be reliable, however, we cannot represent that it is accurate or complete. It is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views are those of the author, Financially INsync Team, and not necessarily those of Raymond James Ltd. Investors considering any investment should consult with their Investment Advisor to ensure that it is suitable for the investor’s circumstances and risk tolerance before making any investment decision. Statistics, factual data and other information are from sources believed to be reliable but accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James Ltd. is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities.

Raymond James Ltd. is a Member Canadian Investor Protection Fund.

Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd., member FINRA/SIPC.